Rules Accumulate. Mechanisms compound.

ODR (Order Defect Rate) is a margin problem caused by decisions compliance does not control

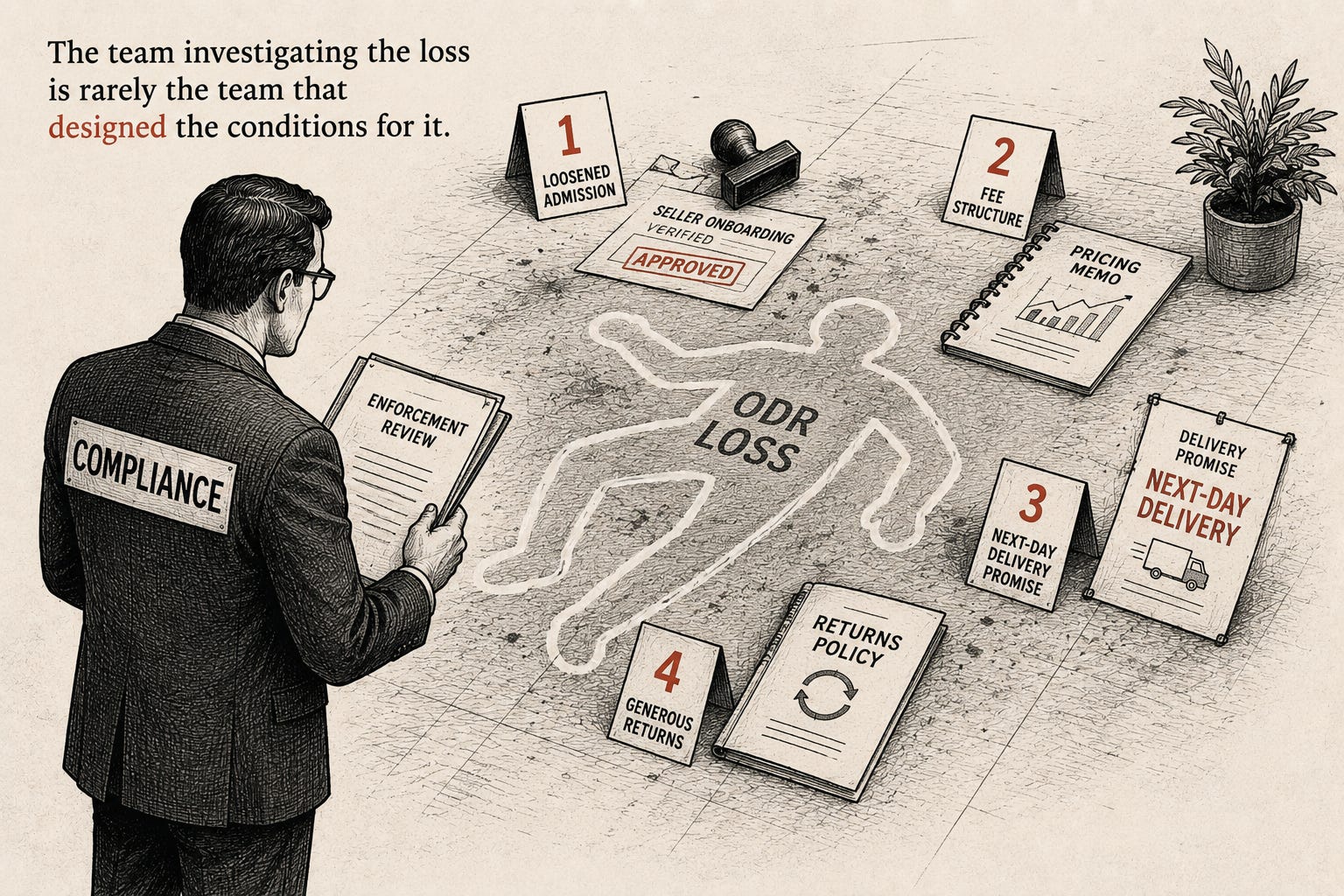

Late in any quarter at a large marketplace, there is a moment the compliance team knows well. The dashboard refreshes. The order defect rate is up. The response is immediate and practiced: identify the sellers above threshold, run the review queue, deliver the consequences, move the metric.

This sequence has the texture of competence. It is fast, visible, and produces a countable output. Cases are actioned. Sellers are notified. The metric, at least briefly, responds.

What this sequence cannot see is that the metric moved in response to decisions made twelve months ago.

An admission threshold was loosened when a growth team was under pressure to hit seller acquisition targets. A fee structure change quietly made fulfillment loss-making for an entire price band. A delivery promise was set to match a competitor without checking whether the seller base could actually deliver it.

The enforcement team is fighting a fire set in another building by people who have since moved on. They will fight this fire competently. It will not go out.

This is the central problem with how marketplace risk and compliance is organized: accountability sits furthest downstream from cause. The function that measures and enforces the metric controls almost none of the decisions that generate it.

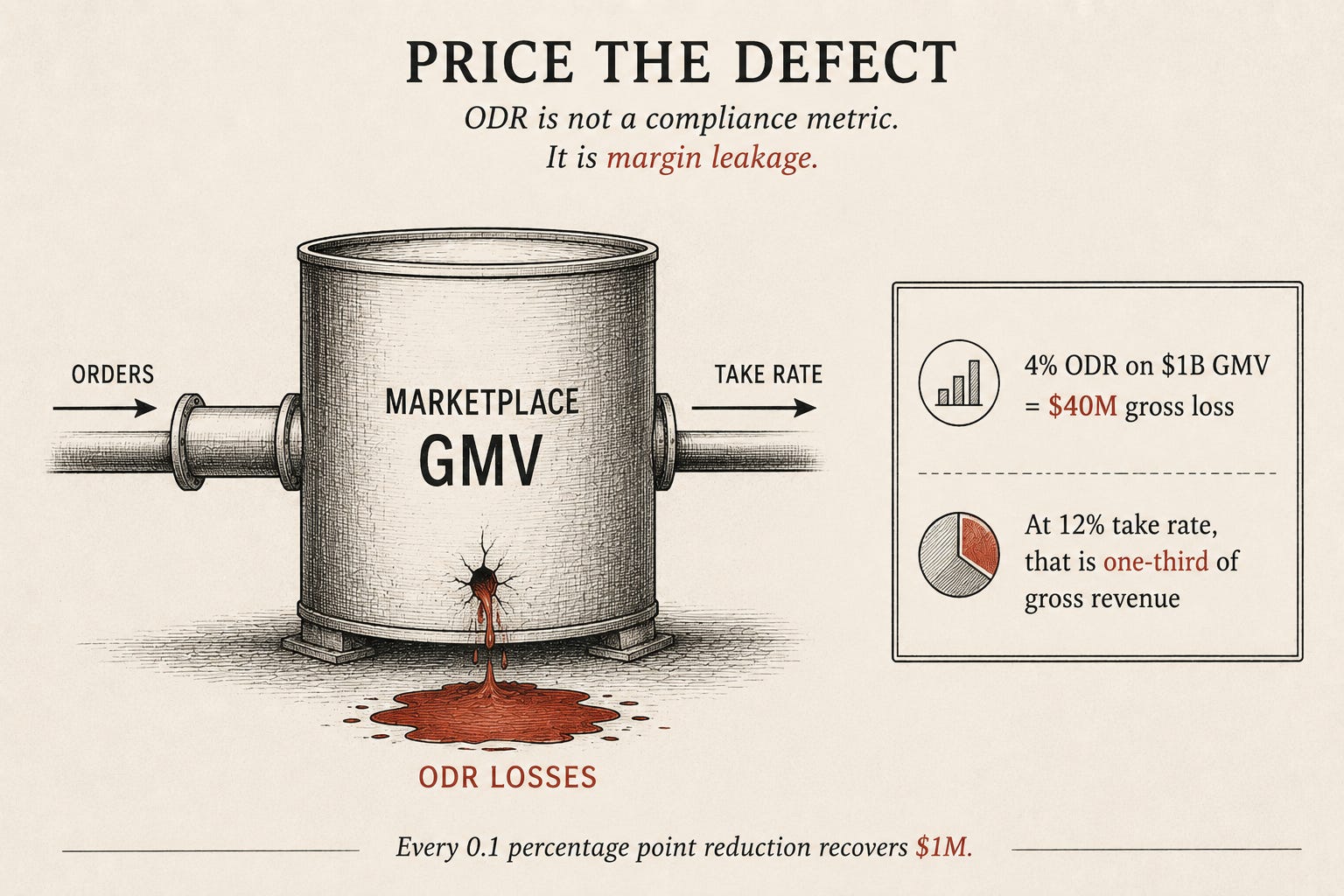

Price the defect

The Order Defect Rate1: cancellations and refunds expressed as a share of platform GMV, is the primary risk metric in most marketplace compliance organizations. It is tracked, reported, benchmarked, and enforced against. What it is not, typically, is priced.

A 4% ODR on a billion-dollar GMV marketplace is forty million dollars in gross losses. At a 12% take rate, that represents a third of gross revenue. Each 0.1 percentage point reduction recovers a million dollars.

That is not a compliance number. It is a P&L number, structurally equivalent to a reduction in take rate, sitting on the books as a cost that is rarely compared against the revenue investments it competes with.

When you translate ODR into dollars and set it next to the GMV growth investment for the same period, the conversation changes. Risk is no longer only a governance function. It is a margin problem. Recognizing it as a margin problem is the prerequisite for everything else.

The safe rule that starved the channel

Some time ago, I joined Tata Tele as a P&L leader and inherited something heavier than a budget: an institutional bias. Channel partners - the distributors who acquired new connections on the ground - were not receiving upfront commissions.

The policy had a history. There had been fraud: channel partners exploiting the arbitrage between upfront commission and activation fee, opening phantom connections to pocket the spread. The response was what risk responses usually are; accurate about the past exploit and blind to the new constraint it would create.

Commissions were restructured to revenue-based payouts. The fraud stopped. The channel started dying.

The problem was structural and invisible. Channel partners are small businesses. Most of them cannot access working capital loans. They need to see profitability every month to pay their people.

A revenue-based commission structure is fine for a large distributor with working capital reserves. For the median channel partner, it was an indefinite deferral of income they could not afford to defer. The policy had eliminated the fraud and replaced it with something quieter and more expensive: a channel that could not move.

I spent the first year of my tenure trying to explain this to Finance and Leadership. We were unable to run sales campaigns. We had marketing support we could not deploy. At the end of that year the report card was unambiguous: acquisition budget under-consumed by 75%, sales targets missed by 50%. The ship was safest in the harbor. But that’s not what ships are meant to do.

The resolution was not to restore upfront commissions wholesale - the original fraud risk was real. The resolution was to build an equation that tested any proposed commission scheme for arbitrage exposure before approval. If the scheme failed the test, it was redesigned. If it passed, it was approved quickly, with the agility the previous regime never had. In the subsequent year we spent 20% less on budget and met our sales targets.

Rules accumulate. Mechanism understanding compounds.

The lesson I carry from that period is not about commissions. It is about the difference between rule accumulation and mechanism understanding.

The commission ban was a rule. It was correct about the mechanism it was designed to prevent and wrong about the mechanism it inadvertently activated. The arbitrage equation was a model of the mechanism itself -- which meant it could be applied prospectively, adapted to new situations, and made faster rather than more restrictive over time.

Rules accumulate. Mechanism understanding compounds.

This distinction is almost entirely absent from how marketplace compliance is designed.

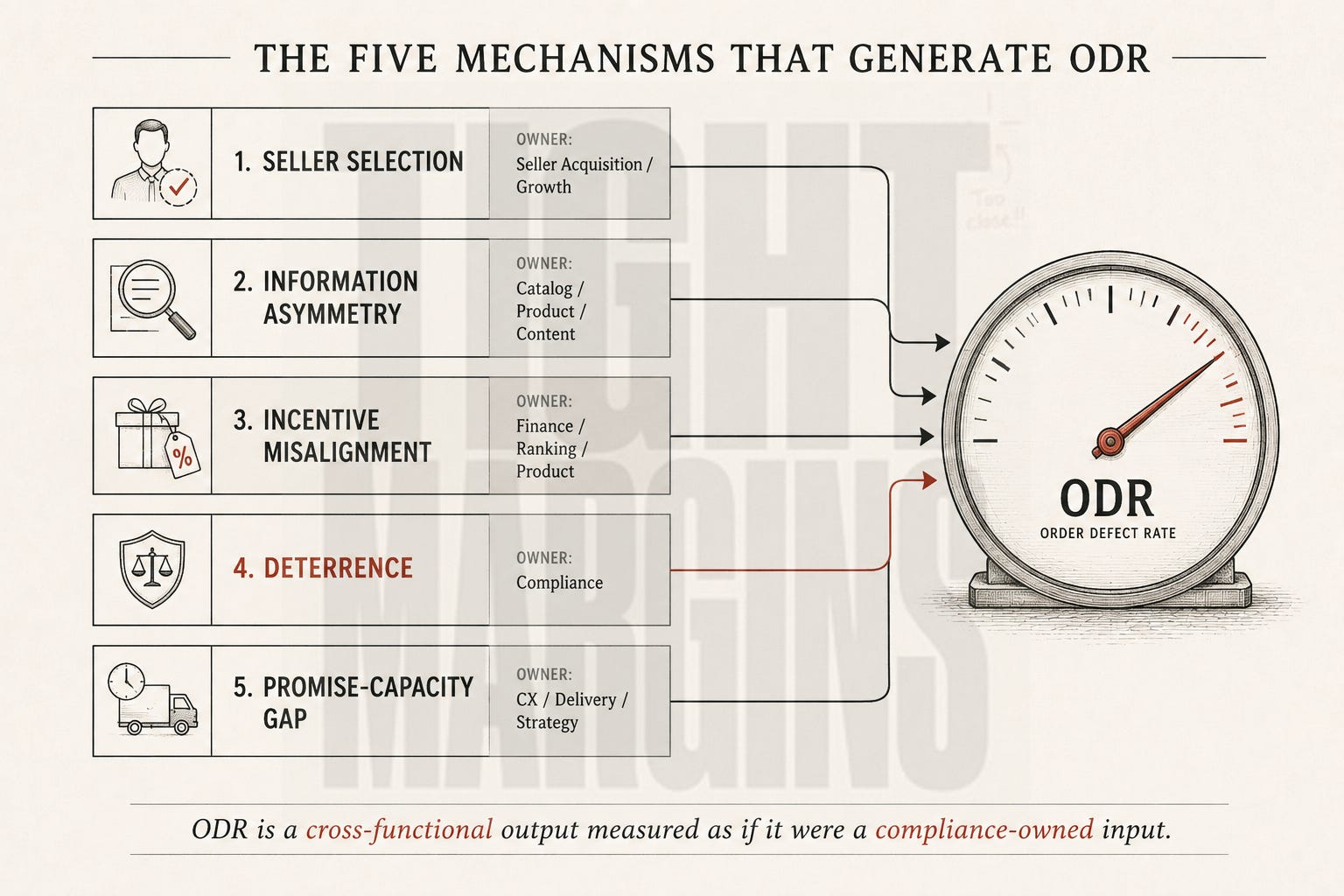

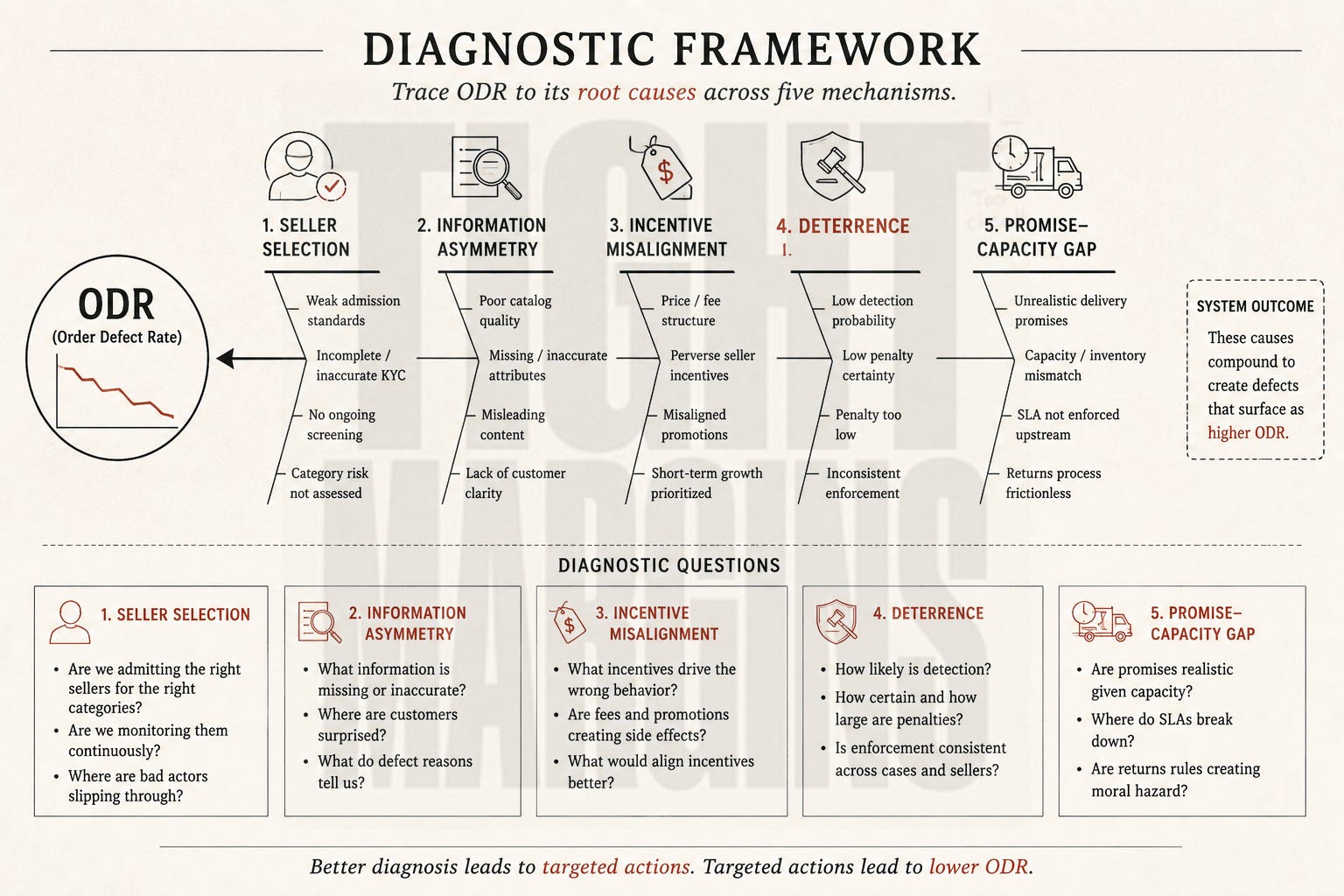

The five mechanisms that generate ODR

The order defect rate is generated by five distinct mechanisms. Each has a separate causal chain. Each has a separate intervention surface.

Selection

The quality of the seller base is set at admission, before any transaction occurs.

Admission quality sets the floor around which all other mechanisms operate.

Information asymmetry

Gaps between what sellers represent and what buyers receive generate returns and claims independently of seller intent.

A seller can generate loss without bad faith if the listing is inaccurate or incomplete.

Incentive misalignment

Sellers respond rationally to fee structures, ranking rewards, and penalty architecture.

If loss-generating behavior is profit-maximizing, loss is what the platform gets.

Deterrence

Enforcement architecture determines whether sellers believe the expected cost of violation is high enough to change behavior.

This is the mechanism compliance most directly owns.

Promise-capacity gap

The platform makes commitments to buyers that a predictable fraction of the seller base cannot execute against.

Losses are then attributed to sellers for a failure caused by platform strategy.

Three of these five mechanisms are generated primarily by decisions made outside the compliance function. The fee structure is Finance’s. The ranking reward architecture is Product and Growth’s. The delivery promise level is Competitive Strategy’s. The return policy is Customer Experience’s. The admission threshold is set by whoever owns seller acquisition targets.

Compliance enforces against the outputs of decisions it did not make, using a metric it cannot move at the source.

The accountability inversion

This is the accountability inversion. It is not a design failure; it is the predictable consequence of organizing a marketplace by function and then measuring a cross-functional outcome.

Each team optimizes locally. The order defect rate is what you get at the intersection. The compliance function is the only one measured against the intersection, with authority over approximately one of the five mechanisms that produce it.

The enforcement team is fighting a fire set in another building by people who have since moved on.

Three observations worth treating as laws

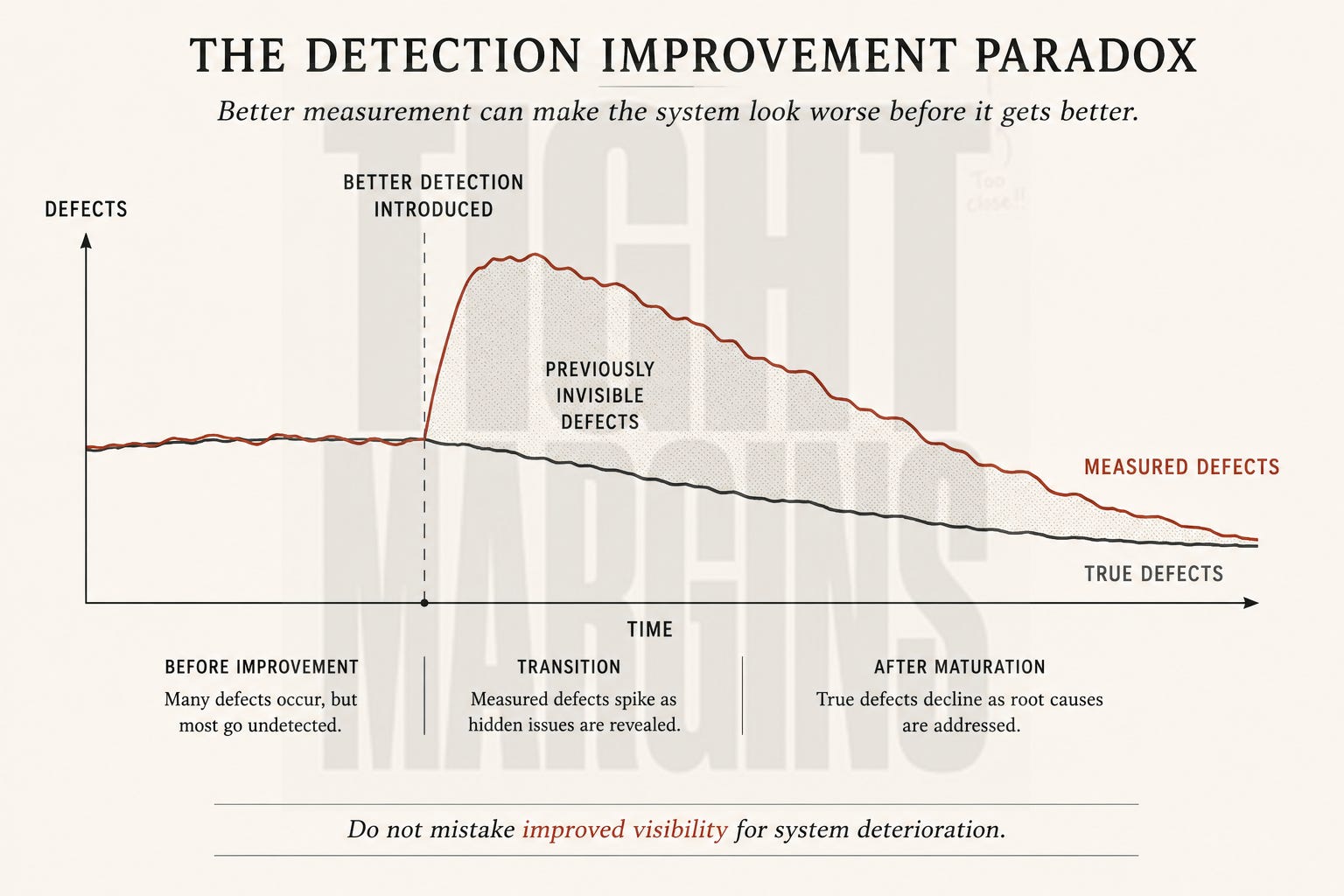

First: the detection improvement paradox.

When a marketplace invests in fraud return detection - building models to identify the returns that are not what they claim to be - the measured ODR gets worse before it gets better. Returns that were invisible in the numerator become visible. The metric, which measures what it can count, reports deterioration.

In a regime where compliance is measured against ODR, this means the measurement infrastructure that would actually improve outcomes looks, at first, like a failure. Platforms that do not understand this dynamic will systematically underinvest in detection because detection looks punitive in the short run.

Better measurement produces worse-looking numbers. Worse numbers produce incentives to avoid better measurement. The trap is self-sealing.

Second: the ratchet asymmetry.

In many marketplaces, ODR appears to degrade several times faster than it recovers. Admitting five hundred high-loss sellers can move the metric within ninety days. Removing their influence through attrition, enforcement, or exit can take four to six cohort cycles to work through the GMV-weighted average.

Launching a delivery promise above the seller base’s capacity widens the gap immediately; recalibrating eligibility takes quarters to propagate. The asymmetry is not behavioral. It is structural, built into the lag architecture of each mechanism. This is not a reason to be fatalistic about recovery. It is a reason to be upstream about prevention.

Third: the lag structure trap.

The five mechanisms operate at different speeds. Enforcement acts within weeks. Information quality acts within months. Selection and promise architecture act over quarters to years.

When ODR deteriorates and the compliance team tightens enforcement, they are pulling the fastest lever against a problem caused by the slowest decisions. The enforcement actions produce observable short-run improvement. The upstream decisions that caused the deterioration are invisible -- they happened a year ago, made by people who have since moved on to other priorities.

Enforcement gets the accountability and the credit. The decisions that actually drove the outcome get neither. Repeat this cycle for three years and you have an organization that is very good at enforcement and chronically unable to understand why the defect rate keeps coming back.

The parallel to the channel commission story is exact. The commission ban was enforcement against a past exploit. It was fast, visible, and produced an observable output: the fraud stopped. What it could not see was the channel starvation building over the following months.

The mechanism it inadvertently activated was slower, quieter, and did not show up in the fraud metric it was designed to move. By the time it appeared in acquisition numbers, the team responsible for the commission structure had no causal model for what they were looking at.

Diagnose before you reorganize

There is a version of this argument that concludes with a prescription: restructure accountability, distribute ODR ownership to the teams generating it, redefine compliance as a risk governance function rather than an enforcement function.

That version is correct and, in most marketplace organizations, politically very difficult. The structural change required is not a process change -- it is a power change.

Attaching ODR accountability to finance teams means finance teams get measured against a number they have historically been able to externalize. Attaching it to growth teams means admission quality becomes a constraint on seller acquisition targets. These are not comfortable renegotiations.

But there is a prior step that does not require political capital: understand what fraction of current ODR each mechanism is generating. This is analytical work, not organizational work.

Start with four diagnostic cuts:

Build the seller cohort matrix: defect rate at ninety days post-onboarding, by cohort quarter, to see whether new cohorts are better or worse than prior cohorts at equivalent age.

Disaggregate returns by reason code to see what share is driven by listing inaccuracy, buyer behavior, or policy generosity.

Plot the seller defect-rate distribution to see whether a spike just below the enforcement threshold is evidence of threshold management rather than genuine quality improvement.

Compare sellers enrolled in fast-delivery programs with non-enrolled sellers of equivalent profile to test for a promise-capacity gap.

This analysis, done rigorously, will tell you where the problem actually lives.

New cohorts are worse at 90 days → Selection problem → More enforcement will not close it. Tighten admission quality, probation, or early-life monitoring.

Defect-rate distribution spikes just below threshold → Incentive misalignment → A continuous penalty function will do more than a lower threshold.

ODR is structurally higher in fast-delivery enrollment → Promise-capacity gap → Actioning sellers may shrink the pool, create pressure to re-enroll marginal sellers, and recreate the failure rate.

The first move is not to reorganize the company. That is usually where good ideas go to be converted into steering committees. The first move is to decompose ODR by mechanism.

Enforcement is necessary. It is not sufficient.

The argument is not that enforcement is wrong. The deterrence mechanism is real and necessary. A platform that does not action violations loses the credibility that makes deterrence function.

That credibility depletes faster than it accumulates. One visible unactioned violation updates every seller’s estimate of the consequences downward, and rebuilding that estimate takes more consistent enforcement than it took to establish it in the first place.

Enforcement is necessary. It is not sufficient.

And in the specific case where the promise-capacity gap is the primary mechanism, enforcement is actively counterproductive: it removes sellers from programs, shrinks the eligible pool, creates enrollment pressure at the margin, and regenerates the structural gap the enforcement was designed to close.

The question every compliance system should ask

The ship that stays in harbor is safe. It is also not a ship anymore, in any meaningful sense. The commission ban at Tata Tele was safe. It was also starving the channel.

What made it workable again was not removing the safety constraint but understanding the mechanism well enough to apply it precisely rather than broadly -- the arbitrage equation, not the commission ban. Rules applied broadly accumulate and constrain. Mechanism understanding applied precisely adapts and unlocks.

Marketplace compliance systems are built from accumulated rules, each correct about the exploit that generated it.

The question worth asking of any such system is not whether the rules are right. It is whether the mechanism that generated each rule still operates the way it did when the rule was designed -- and whether the aggregate effect of the rule set, across all five mechanisms, is reducing loss or redistributing it.

A mature marketplace risk question is not, “Which sellers crossed the threshold?” It is, “Which upstream decision made threshold-crossing economically rational, operationally likely, or structurally unavoidable?”

Until that question is asked, compliance will keep maintaining very safe harbors full of ships that have not sailed in years.

I will publish a companion piece applying the same framework to agentic AI trust this Thursday.

Measurement note: industry-standard ODR is usually expressed as defective orders divided by total order count. This article uses a GMV-weighted formulation because it better captures the economics at stake: a seller with many low-value cancellations and few high-value ones looks different on a GMV basis than on an order-count basis.